More than just a score

Monitor your credit score, get alerts and find personalised credit card and loan offers to help you live your financial best.

*Free for 30 days then £14.95 a month.

Cancel anytime.

Report & Score updated daily upon login

Traffic light system, identifying parts that need attention

Actionable hints and tips within your report

24/7 Identity protection tools

FREE Rewards card

Marketplace

In partnership with

Compare loans, credit cards and car finance

Features of the Equifax Credit Report & Score

Explore the features and benefits of the Equifax Credit Report & Score

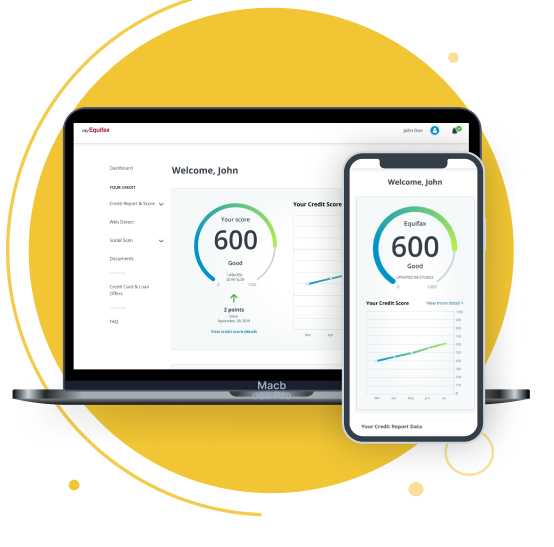

Access to your credit report & score

Get a detailed view of your credit report and credit score out of 1000 with Equifax Credit Report & Score.

Protect your identity

Equifax can help you keep your identity safer. As part of your Equifax Credit Report & Score, WebDetect alerts you if it finds your financial details on websites used by fraudsters to trade personal information.

A free 12 month tastecard including Coffee Club

With all our paid subscriptions, you’ll receive a digital 12 month tastecard giving you access to discounts and offers on dining, coffee, pizza delivery, cinema and days out (access removed after cancellation).

Our Services

Family & Friends Plan

All the benefits of Equifax Credit Report & Score for up to 3 users, potentially saving £240 per year! Great for those making financial decisions together or simply looking out for loved ones.

Equifax Credit Report & Score

A detailed view of your enhanced credit report and score out of 1000. Also included are a range of Identity Protection features to help safeguard your information.

Statutory Credit Report

Your free statutory credit report shows you the information Equifax has about your credit history.

*Your first 30 days are free then it’s £22.95 a month for Equifax Family & Friends Plan or £14.95 a month for Equifax Credit Report & Score. You can cancel at any time.

From onboarding to offboarding

Practical tips on everyday money matters

Start your journey towards better financial well-being with our straightforward, jargon-free guidance. Find useful information and tips and tricks on a range of financial subjects.

Read what our customers have to say

Frequently asked questions

A credit report is a detailed record of your credit history. It includes information about your credit accounts and past payments, among other things. Lenders use this report to assess your creditworthiness for things like new credit cards, loans or mortgages. Doing a credit check is an important step towards understanding your credit history.

Your Equifax Credit Score is between 0-1000 and is calculated using the information within your credit report. A variety of factors can affect your credit score. These include timely payments, credit utilisation, new credit accounts, and your history of credit repayment.

Credit scores can change whenever new information is added to your credit report. This can happen any time a creditor reports something about your account. Therefore, your credit score can technically change as frequently as daily.

Your Equifax Credit Report will refresh when you log on, a maximum of once a day, to reflect any changes to your credit information.

Your Equifax Credit Report will refresh when you log on, a maximum of once a day, to reflect any changes to your credit information.

Yes, checking your own credit score is considered a "soft inquiry" and does not affect your credit score. However, "hard inquiries", which is when a lender checks your credit due to an application for credit, may impact your score.

You can improve your credit score by making timely payments, reducing the amount of debt you owe, not opening unnecessary new credit lines, and regularly checking your credit reports for accuracy.

Equifax Report and Score makes taking control of your credit report and scores easy and straightforward. Get your free credit score and free credit check today.

Equifax Report and Score makes taking control of your credit report and scores easy and straightforward. Get your free credit score and free credit check today.

Most negative information, like late payments, will stay on your credit report for seven years. Some serious negative information, such as certain bankruptcies, can stay on your report for up to 10 years.